This contribution by Susan Shaheen and Adam Cohen in which they pick out and analyze some of the main trends and eventual future prospects of the carshare "industry" in North America is the second country report in this World Streets 2013/14 series updating our readers on the latest developments internationally in this fast-moving, fast-developing field of new ways of owning and using cars. To access all the reports in this series thus far, you are invited to click to http://worldstreets.wordpress.com/category/carshare/

North American Carsharing Market Trends

By Susan Shaheen, Ph.D. and Adam Cohen. Autumn 2013.

Transportation Sustainability Research Center -University of California, Berkeley

North America reaches 1 Million Carsharing Members

As carsharing matures, a key question remains: how will it scale into less dense areas? What role will new entrants and business models play in its expansion? How will it be branded to be successful and for which market segments? What social and environmental impacts can be expected as it expands and by approach over time? What role should public policy play in supporting its expansion? What innovative insurance models could be developed to support shared use? What type of service integration would best support shared vehicles and the sharing economy overall? All of these questions are outstanding, but answers are beginning to unfold as this evolution continues.

Growth of Automakers, One-Way, and Car Rental

In North America, two automaker programs (car2go and DriveNow) represented 11.7% and 18.4% of the carsharing membership and fleets deployed, respectively, in January 2013. In December 2012, Daimler’s car2go carsharing program expanded operations into Seattle. One-way (or point-to-point) carsharing allows members to pick-up a vehicle at one location and drop it off at another. As of June 2013, car2go and DriveNow collectively operated one-way carsharing services in eight American markets in the U.S. (Austin, Denver, Miami, Portland, San Diego, San Francisco, Seattle, and Washington, D.C.). As of June 2013, car2go operated in three metropolitan markets in Canada (Calgary, Toronto, and Vancouver). In May 2013, Communauto announced plans to launch an electric one-way carsharing pilot between June and October 2013 in the Plateau-Mont-Royal borough of Montreal. In June 2013, Indianapolis, IN announced that it plans to launch an EV one-way carsharing service of 500 vehicles in partnership with the Bolloré Group (the founders of Autolib in Paris) in Spring 2014.

In North America, rental car programs represented 79.0% and 63.1% of the carsharing membership and fleets deployed, respectively, in January 2013. This represents an increase from 15.8% of membership and 11.8% of fleets in January 2012, largely due to the Avis Budget Group acquisition of Zipcar, which was announced on January 2, 2013. Note this does not reflect the May 2013 acquisition of IGO CarSharing by Enterprise Holdings.

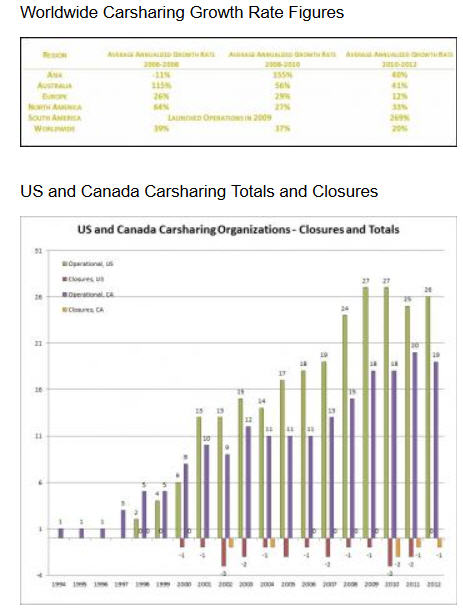

Since 1994, 75 carsharing programs have been deployed in North America—46 are operational and 29 defunct. As of January 1, 2013, there were 20 active programs in Canada, 25 in the United States (U.S.), and one in Mexico, with 1,033,564 carsharing members sharing 15,603 vehicles in North America. The three largest providers in the U.S. and Canada support 88.8% and 80.8% of total membership, respectively.

As of January 1, 2013, 20 Canadian operators claimed 141,351 members and shared 3,432 vehicles. In the U.S., 891,593 members shared 12,131 vehicles among 25 operators. In Mexico, 620 members shared 40 vehicles among one operator. (Note: multi-national programs with operations in both the U.S. and Canada are counted as an individual operator in each country. Also, the histogram on Pg. 4 reflects a vehicle decline in the U.S. between July 2012 and January 2013. This has occurred for the past four seasons, as a few large programs seasonally reduce their fleets in the winter months.) Between January 2012 and January 2013, carsharing membership grew 24.1% in the U.S. and 53.4% in Canada. Additionally, between January 2012 and January 2013, carsharing fleets grew 23.6% in the U.S. and 35.9% in Canada.

Member–vehicle ratios are an important metric, which can be used to assess how many customers are being served per vehicle and the relative usage level of carsharing members. As of January 2013, U.S. member-vehicle ratios were 73:1, representing a 0.4% increase

between January 2012 and January 2013. In Canada, the ratio was 41:1 representing a 12.9% increase over this same period. Measured from January-to-January, Canadian member-vehicle ratios have risen for seven consecutive years. In January 2013, North American member-vehicle ratios increased to 66:1, representing an increase of 0.8% from January 2012.

In January 2013, U.S. for-profit programs (12 of 25) represented 48% of the operators and accounted for 95.7% of the members and 93.1% of vehicles. In Canada, for-profit programs (8 of 20) represented 40% of the operators and accounted for 92.3% of the membership and 89.1% of the fleets deployed.

Personal Vehicle Sharing

Shared-use vehicle services have entered a new phase of development characterized by short-term access to privately-owned vehicles, referred to as personal vehicle sharing. Broadly speaking, personal vehicle sharing companies broker transactions among car owners and renters by providing the organizational resources needed to make the exchange possible (i.e., online platform, customer support, auto insurance, and technology). In May 2013, RelayRides acquired Wheelz. As of June 2013, there were 9 personal vehicle sharing operators in North America (1 of 9 in pilot phase), three planned, and eight defunct in North America.

North American Carsharing Market Trends

*Data depicted July of each year, except for January 2013. Our numbers do not include p2p. The operators will not provide these data.

Industry Innovations

Communauto Offers Members GHG Emission Offsets

In April 2013, Communauto, operating throughout the Province of Québec, launched a voluntary program to enable its members to voluntarily purchase carbon credits in partnership with Planetair and CO2 Environnement. Based on per-kilometer use, Communauto offers three different offset rates depending on the vehicle driven (electric, hybrid, or gas). The carbon offsets will be used for reforestation projects in Québec and to support international renewable energy and energy efficiency projects.

City CarShare Expands Wheelchair Accessible Carsharing

In 2008, City CarShare of the San Francisco Bay Area introduced the nation’s first wheelchair accessible carsharing vehicle in partnership with the City of Berkeley’s Commission on Disability. In January 2013, City CarShare expanded this program with two additional wheelchair accessible minivans. Each minivan holds two people using mobility devices, plus a driver and three additional passengers depending on the size of the wheelchair(s) [Pictured lower left].

IGO CarSharing Installs Solar Canopies

In November 2011, IGO CarSharing in Chicago, IL launched a $2.5 million electric vehicle (EV) project to expand its fleet with an additional 36 EVs and the installation of 18 solar-powered charging stations. The solar canopies represent an industry milestone to provide clean energy to charge their solar fleet. Through a public-private partnership, IGO’s solar canopies also offers a limited number of charging stations available for public use. Construction of the canopies is ongoing [Pictured lower right].

Thoughts On Carsharing and Car Rental Mergers/Acquisitions

The recent acquisitions of IGO CarSharing by Enterprise Holdings in May 2013 and Zipcar by the Avis Budget Group in January 2013 continues a trend of mergers and acquisitions in North American “classic” carsharing (or roundtrip, short-term vehicle access). This trend began in the early 2000s with the Flexcar acquisition of CarSharing Portland in 2001 and the merger of Zipcar and Flexcar in 2007. Mergers and acquisitions again became an industry hallmark with the Enterprise Holdings’ acquisition of PhillyCarShare in 2011 and their acquisition of Mint Cars On-Demand in 2012.

Announced in January 2013, Avis Budget Group officially completed the $500 million acquisition on March 14, 2013. Avis, as a brand, had an early history in short-term hourly rentals. Avis-Europe became the first large-scale rental car company to launch carsharing servicesnotably CARvenience, which started operations in the United Kingdom in 2001. Despite its early entry into carsharing, these efforts were small scale and by the end of the decade were eclipsed by the larger entries of Enterprise, Hertz, Sixt, and U-Haul until its acquisition of Zipcar.

Based on data from Auto Rental News, the table to the right represents the top four car rental companies compared to Zipcarboth in fleet size and revenue. In terms of fleet scale, Zipcar represents 0.5% of the top four rental car fleets and less than 3% of the Avis Budget Group’s fleet size in 2012. Note, Auto Rental News did not publish disaggregated data for other carsharing operators in 2012.

Studies on “classic” carsharing have emphasized the benefits attributed to neighborhood-based carsharing. This model has documented that each carsharing vehicle reduces the need for 9 to 13 private automobiles in North America through both vehicle sales and foregone purchases due to carsharing. A survey of members of all major North American carsharing organizations in Fall 2008 (6,281 respondents) found an average vehicle miles/kilometers decline per year of 27% (observed impact, based on vehicles sold) and 56% (full impact, based on vehicles sold and postponed purchases combined) in the before-and-after mean driving distance. This equates to an aggregate reduction of 1.1 billion miles driven for members of classic neighborhood carsharing (as of January 1st, 2013). However, this is still relatively small compared to the Federal Highway Administration estimate of 2.9 trillion miles driven in the U.S. in 2012.

Finally, approximately 25% of respondents sold a vehicle, and roughly another 25% of the total sample would have considered obtaining a vehicle, if carsharing disappeared. These two subgroups were mutually exclusive; those that shed a vehicle were not counted among those who would consider acquiring a vehicle. In total, the survey suggested that about 50% of members had either shed or forgone the acquisition of a vehicle as part of their carsharing membership (1-3).

As of January 2013, there were 46 carsharing operators in the U.S., Canada, and Mexico serving approximately 1,033,564 carsharing members, with a combined fleet of 15,603 vehicles in North America (excluding peer-to-peer carsharing). In January 2012, North American rental car programs represented 15.8% of the membership and 11.8% of the fleets deployed. In January 2013, rental car programs had increased their market share to 17.1% and 13.1% of the carsharing membership and vehicles deployed (before the Avis acquisition of Zipcar, which was announced on January 2, 2013). With the Avis-Budget acquisition of Zipcar, the smallest rental car brand in carsharing (Avis has a small presence in Europe) became the largest. Following the acquisition of Zipcar by Avis, rental car brands now comprise 79.0% and 63.1% of the carsharing membership and fleets in North America, respectively (based on January 2013 numbers – excluding Enterprise’s recent acquisition of IGO). Enterprise Holdings acquired three carsharing organizations between 2011 and 2013 in addition to its own service.

Since carsharing launched in North America in 1994 (Montreal, Canada), it has continued to grow and evolve. Today, there are many new players (including automakers); more advanced technologies for managing operations, reservations, and billing; and new business models. Innovative models include one-way carsharing or point-to-point services (such as Daimler’s car2go, BMW’s DriveNow, and Communauto’s electric one-way carsharing pilot program) and peer- to-peer carsharing (e.g., Getaround and RelayRides). Peer-to-peer or personal vehicle sharing occurs when privately-owned vehicles are made temporarily available for shared use. Other models will soon be on the horizon, such as fractional ownership (i.e., individuals sub-lease or subscribe to a vehicle owned by a third party).

A key question is how carsharing will impact car rental and how car rental will impact carsharing. We believe that the answer is both and that some of the implications and trends might include the following in the shorter and longer term. It is likely the car rental industry will continue to enhance customer convenience through increased automation, unattended services, and virtual storefronts.

Operations

- Continued blurring between clear definitions of “carsharing” and “car rental,” as the latter continues to provide hourly rental services and in some instances “unattended car rental services,” sometimes with and without insurance and gas.

- Implementation of pre-qualified or pre-approved car rental users and the implementation of virtual storefronts. This would likely include greater deployment of “unattended access” in the rental industry to enhance customer convenience and increase profit margins by reducing or eliminating the expenses associated with maintaining personnel at storefronts or airport locations. “Virtual agents,” self-service kiosks, and unattended access have already been piloted and deployed by a number of rental car companies in select locations including the Avis Budget Group, Enterprise Holdings, and Hertz, for instance.

- Increased access. By eliminating “attended access,” car rentals can provide enhanced services (longer hours, increased locations, etc.) without having to provide personnel with their vehicles. Additionally, there might be an increase in the number of rental locations, since new locations not previously profitable could now forgo associated storefront expenses.

- Uniform age for insurance of carsharing and rental cars. Generally, the standard age for carsharing use in the United States is 21 with special provisions for drivers between 18 and 20. In Canada, the typical age for carsharing is 25. At present, there are different policies for renting vehicles, if you are under 25 years of age. This can be a concern among the college/university demographic market. One thing that might happen in the future is a reduction in the minimum age for rental car use, along with the possible application of additional insurance costs for carsharing drivers under the age of 25 to account for increased risk. This could come in the form of a monthly fee or even in a slightly higher hourly or mileage rate for use.

- Experimentation in insurance models, such as pay-as-you-drive or usage-based insurance, to reduce costs and provide shared- use vehicle policies crafted to protect its users and vehicle providers.

- Potential blurring of carsharing and rental car business models. In March 2013, Avis announced that it would deploy Zipcars at New York City airports, offering hourly and daily rates. It is important to note, however, that just as carsharing has sub-markets (e.g., one-way, neighborhood, and peer-to-peer), rental cars have sub-markets as well (e.g., airport, neighborhood, and moving/storage).

Technology

- Incorporation of carsharing telematics technologies by automobile manufacturers. This would most likely occur in fleet vehicles first. Historically, vehicle manufacturers have been adverse to “buying-back” vehicles that have been adapted with third-party technologies. However, with the entry of automakers into carsharing (e.g., car2go and DriveNow), telematics technology could be factory-equipped in fleet vehicles. We have seen the beginning of this trend with General Motor’s use of OnStar to support RelayRides. In the longer term, depending on the growth of peer-to-peer or personal vehicle sharing consumer vehicles could also be equipped with optional in-vehicle telematics direct from the factory (in contrast to after-market technology).

- Incorporation of telematics technology across entire rental car fleets to facilitate vehicle cross-flow between carsharing and traditional rental services and added flexibility to use an entire fleet for daily, hourly, attended-access, and unattended-access as vehicle demand for these services fluctuates.

- Linkage to connected car technologies. Carsharing fleets will be increasingly connected to the Internet, “cloud,” and sensor networks. Such technologies can aid in improved vehicle operations, as well as ecodriving (more efficient routing to avoid traffic, steep inclines, or stops at traffic signals).

- Connection to autonomous vehicles. Linkage between carsharing fleets and autonomous vehicles (or self-driving), such as self-parking, self-recharging in the case of electric vehicles, and to some extent self-driving.

Some Final Thoughts and Questions

As carsharing matures, a key question remains: how will it scale into less dense areas? What role will new entrants and business models play in its expansion? How will it be branded to be successful and for which market segments? What social and environmental impacts can be expected as it expands and by approach over time? What role should public policy play in supporting its expansion? What innovative insurance models could be developed to support shared use? What type of service integration would best support shared vehicles and the sharing economy overall? All of these questions are outstanding, but answers are beginning to unfold as this evolution continues.

References:

(1) Martin, Elliot and Susan Shaheen. “Greenhouse Gas Emission Impacts of Carsharing in North America.” IEEE Transactions on Intelligent Transportation Systems, Volume 12, Issue 4, p. 1074-1086 (2011).

(2) Martin, Elliot, Susan Shaheen, and Jeffrey Lidicker. “Impact of Carsharing on Household Vehicle Holdings: Results from North American Shared-Use Vehicle Survey,” Transportation Research Record, No. 2143, p. 150-158 (2010).

(3) Martin, Elliot and Susan Shaheen. Greenhouse Gas Emission Impacts of Carsharing in North America. Research Report 09-11. San Jose: Mineta, Transportation Institute (2010).

# # #

About the authors:

Susan Shaheen is Co-Director of the Transportation Sustainability Research Center (TSRC). She has a Ph.D. in ecology, focusing on technology management and the environmental aspects of transportation, from the University of California, Davis and a MS in public policy analysis from the University of Rochester.She was the chair of the Emerging and Innovative Public Transport and Technologies (AP020) Committee of the Transportation Research Board (2004 to 2011) and served as the founding chair of the Carsharing/Station Car TRB Subcommittee from 1999 to 2004. Since 2004, Shaheen has been a research associate with the Mineta Transportation Institute at San Jose State University.

Susan Shaheen is Co-Director of the Transportation Sustainability Research Center (TSRC). She has a Ph.D. in ecology, focusing on technology management and the environmental aspects of transportation, from the University of California, Davis and a MS in public policy analysis from the University of Rochester.She was the chair of the Emerging and Innovative Public Transport and Technologies (AP020) Committee of the Transportation Research Board (2004 to 2011) and served as the founding chair of the Carsharing/Station Car TRB Subcommittee from 1999 to 2004. Since 2004, Shaheen has been a research associate with the Mineta Transportation Institute at San Jose State University.Adam Cohen joined the suite of projects at TSRC as an undergraduate student

researcher in Fall 2004. His early TSRC research projects included the technical and legal feasibility of automated speed enforcement (ASE). As an undergraduate, Adam studied legal studies and urban studies at UC Berkeley and is interested in pursuing a career in transportation engineering. Graduate courses in Civil Engineering, Transportation Engineering and City and Regional Planning augment his ongoing research. Currently, Adam has focused his research on North American and world carsharing. Adam received both the 2004 & 2005 Bay Area ITE Scholarship Essay Award, and was the 2005 District 6 Institute of Transportation Engineers (ITE) Fellow.

researcher in Fall 2004. His early TSRC research projects included the technical and legal feasibility of automated speed enforcement (ASE). As an undergraduate, Adam studied legal studies and urban studies at UC Berkeley and is interested in pursuing a career in transportation engineering. Graduate courses in Civil Engineering, Transportation Engineering and City and Regional Planning augment his ongoing research. Currently, Adam has focused his research on North American and world carsharing. Adam received both the 2004 & 2005 Bay Area ITE Scholarship Essay Award, and was the 2005 District 6 Institute of Transportation Engineers (ITE) Fellow.About TSRC

The Transportation Sustainability Research Center (TSRC) was formed in 2006. TSRC is managed by the Institute of Transportation Studies of the University of California, Berkeley; it is headquartered at the university’s Richmond Field Station. TSRC uses a wide range of analysis and evaluation tools, including questionnaires, interviews, focus groups, automated data collection systems, and simulation models to collect data and perform analysis and interpretation of the data. The center develops impartial findings and recommendations for key issues of interest to industry and policy makers to aid in decision making. TSRC has assisted in developing and implementing major California and federal regulations and initiatives regarding sustainable transportation, including zero emission vehicle credits for carsharing vehicles as part of the Zero Emission Vehicle (ZEV) Mandate in California.

- - > For more from their programs: http://www.imr.berkeley.edu and http://www.tsrc.berkeley.edu.

# # #

Print this article

Print this article

[…] See on worldstreets.wordpress.com […]

ReplyDelete